What Are the 10 Best Savings Accounts?

Saving money often proves to be difficult for some people. I completely understand. I admit, saving money, while I do it, is not the highest on my priority list. It should be higher, I know. It is something I struggle to do. To me, it is a balance between having what I want now versus saving money for a future that may never come.

Meet the Wealthry Store.

Make Smart Financial Decisions, Starting NOW.

Top 10 Savings Accounts

What I have come to find over the years, the best way is to balance having some of the things you want right now and saving for your future. The reality is people are living longer and medical expenses continue to rise. It makes sense that you have money in the bank for those needs. It takes some money handling skills to find a good balance.

Do not fear, it does not take a huge amount of skill, but knowledge is power. Continue reading to find out more about managing money and the best savings accounts to grow your money.

What Is a Savings Account?

I know you must be thinking, "of course I know what a savings account is and you do not need to tell me." I would imagine on the most basic level, you do know that a savings account is an account at a bank where you put money to store it. I want to dig a little deeper into the definition of a savings account so you can truly understand what it is. Most importantly, you can understand how a savings account can help you.

Your money can grow when it is in a savings account because it accrues interest. The money that you put in your savings account is insured by the federal government for as much as $250,000. If anything happens to the bank where your money sits, up to $250,000 is safe. It is much safer than that shoebox you keep your money in now.

Online Banking

You can access some of the best savings accounts online. The world of savings accounts is literally at your fingertips. All you need to do is just a little research and you can find information about the best savings accounts, after you read this article, of course. Virtually every bank has a website today. While most of them have some type of mobile banking, each one has a varying level of mobile access.

When you look for the best savings accounts for you, be sure that they provide services in the way you want to use them. For example, if you prefer to go into the bank and talk to someone, make sure the bank you select offers those options. Now, let’s take a look at our top savings account choices:

Top 3 Savings Accounts

There are many options available on the market today when you are looking for the best savings accounts. I am going to list ten of them for you in this article spread out over the next few sections. Each of these accounts has something different to offer to you. Make sure whichever account you select has all of the features in which you are interested.

1. CIT Bank

The first bank I would like to talk about is the CIT Bank and their CIT Bank Savings Builder Account. This account has a 2.10 percent interest. This is one of the highest interest rates you will find. There are certain criteria that you must meet to gain the 2.10 percent interest rate. You do not, however, have to have a high balance to get the rate. They have a low minimum amount to open the savings account. You earn interest on your entire balance in the account. They do not have checking accounts. They have options for online accounts. Their website is simple to use and you can sign up for a new account easily.

2. Discover Bank

The second bank I want to mention is Discover Bank. They are a well-established bank that has been around for a long time and has offered an online platform for quite some time. They are known foremost for their credit cards, but they are just as solid as a bank. They offer 1.85 percent interest on their savings account. Discover does not have a requirement for a minimum balance. They do not have any fees. Discover is offering a special through the middle of November 2019. If you deposit $15,000, they give you $150 and if you deposit $25,000, they give you $200.

3. Betterment

The third bank I want to mention is Betterment and their Betterment Everyday account. Right now, they only offer a savings account; they do not have checking accounts at this time. They do, however, have a waitlist for their checking account. Their current interest rate is 2.04 percent and they do not have a minimum balance or fees. Their accounts are FDIC insured for as much as $1,000,000.

Next 3 Savings Accounts You Want to Consider

There are still more banks that offer the best savings accounts, depending on your needs. I would recommend that you check out the websites of all the banks before you make your final selection. See how easy it is to move around their site and find the information you need. Make sure the bank fits you. There are so many from which you can choose that you do not have to settle.

4. UFB Direct

The fourth bank is UFB Direct, which offers you a tiered type of savings account. If you maintain a balance of $10,000 or more, you have an interest of 2.15 percent. However, if you do not have a balance of at least $10,000, you get 0 percent interest. Yes, that is correct 0 percent interest. If you decide to go with this account, you should plan to keep $10,000 or more in the account. They have no maintenance fees which keeps them as an option providing you plan to keep a high balance.

5. Goldman Sachs

The fifth bank is Goldman Sachs and the Marcus account. This account constantly provides you with high interest rates of around 1.90 percent. It also has no fees and there is no minimum to open the account. They are FDIC insured up to $250,000. They have high amounts that they will allow you to transfer in and out of the account. One downside is they do not have a mobile check deposit feature. The best way to get money into the account is to transfer it from a linked account.

6. SoFi Money

The sixth bank is SoFi Money. This account offers around 1.80 percent interest and is free across the board. There is no minimum to open the account. There is no minimum amount that you have to keep in the account. There are no fees. They do not even have overdraft or ATM fees. One downside is the limit on withdrawals is somewhat low. This account is considered a money market account and is a hybrid between a checking and savings account.

Look At These 2 Next...

Yes, there are still more accounts that might interest you. I warned you that there are a lot of banks that offer some of the best savings accounts. I want to make sure you are well informed so you are able to make the best decision for yourself.

7. Ally Bank

The seventh bank you might want to consider is Ally Bank. This is a completely digital bank, so all interactions occur online. They provide outstanding customer service and their website and mobile sites are easy to navigate. While their savings account is not the highest yielding interest at 1.80 percent, they offer some other perks that may make this bank worth it to you. They do not have a minimum requirement for deposit and there are no monthly maintenance fees. They are a full-service bank with a complete line of money market products, including checking accounts and CDs.

8. HSBC

The eighth bank that I would like to bring to your attention is HSBC. While this bank has been around for quite some time, only recently has it made a name for itself in the US. They are offering an interest rate of 2.05 percent and have no balance minimum. They do not charge any monthly maintenance fees and offer a great online banking experience. They are a full-service bank and they offer a full line of products. If you combine this high yield savings account with their Premier checking account, you may receive a $750 bonus as a welcome.

The Last 2 You Should Consider...

Last but certainly not least, I have two more banks that you should check out before you make your pick among the best savings accounts.

9. Barclays Bank

Ninth on the list is Barclays Bank. While it is most known for its credit cards, it also has high yield savings account with an interest rate of 1.9 percent. Barclays only offers their products in the US. There is no minimum to open the account. The 24-hour access to online banking and direct deposit. They have a mobile app to help you save and deposit and transfer money. Barclays does not offer a checking account or ATM access. This is an online-only bank as they do not have branches.

10. Synchrony Bank

The tenth is Synchrony Bank. This is also an online-only bank. They offer a 1.9 percent interest rate and many other perks. They have excellent customer service and you can contact them via phone or chat every day of the week. They provide identity theft resolution free to their customers along with other discounts. You can upgrade your account to be a Diamond member and unlock even more perks. They reimburse any ATM fees you receive and offer three free wire transfers per month. They do not offer a checking account.

Are There Any Other Ways to Save?

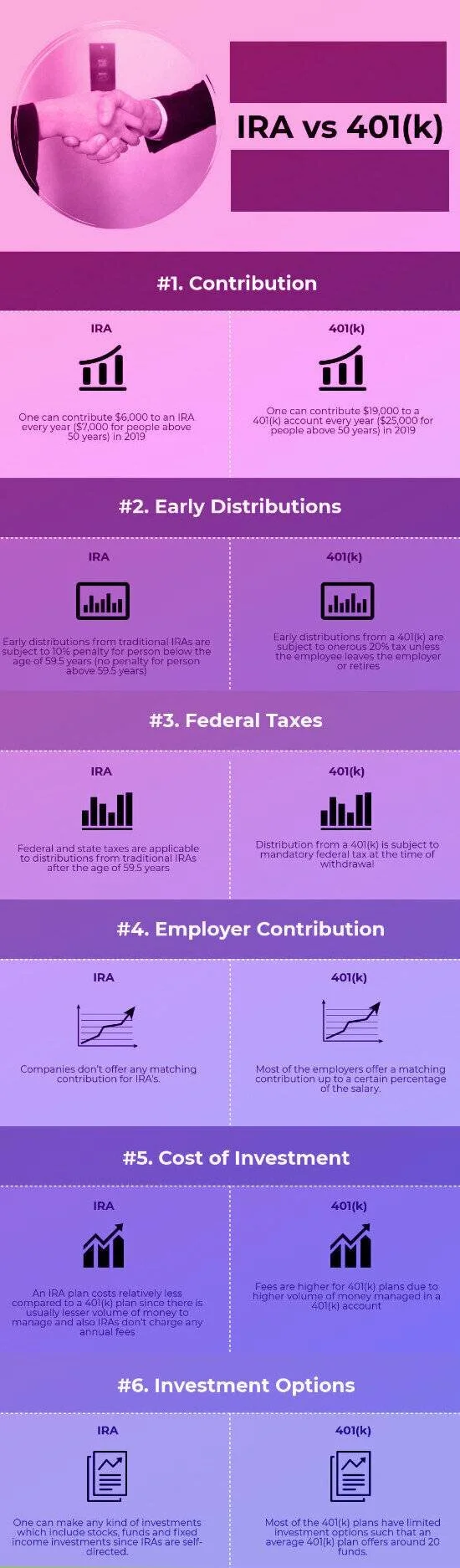

Even though you can find some of the best savings accounts on the market, they are not the only way to save your money. There are some terms that you probably have heard, but you may not really understand them. Terms like IRA, 401k, CDs, and bonds. I am going to give you a high-level explanation of them. This way you can make an educated choice about where you want to save your money.

401k

This is a retirement plan that your employer offers. You select how much money you want withheld from your paycheck each pay period. This money is taken out of your check before it is taxed. That means that the amount of money you earn decreases and makes your taxable income lower. Often employers will match a certain percentage of how much you put into your 401k.

IRA

This is an Individual Retirement Account. This is not offered through an employer. You would go through a financial institution to create an IRA. It can be used as a primary source of saving money for retirement or to supplement a retirement plan offered by an employer. There are a couple of different IRAs from which to choose.

A traditional IRA allows you to contribute regularly which can be deducted on your taxes. The earnings you make on a traditional IRA are taxed when you take the money after retirement. A Roth IRA is also set up through a financial institution but there is no tax break when you make these contributions. The money you earn which you deposit into your Roth IRA is considered income just like any other. A rollover IRA is one you take from one retirement plan and put it into an IRA.

CDs

This is a Certificate of Deposit. You put a certain amount of money into this account for a specified amount of time. It could be anywhere from three months to five years. The more time you leave the money in the account, the higher the interest rate you receive. CDs are insured by the federal government and they are a safe way to invest your money. You are not able to take the money out of the account before the time period expires.

Bonds

The government issues bonds for a set amount of money for a set period of time. When the bonds reached maturity, you get the money back that you paid with interest. The terms are anywhere from ten to fifty years.

What Are the Positives about CDs?

Safe Returns

Certificates of Deposit (CDs) have a long history of safe returns on your investment. You are allowing the bank to use your money in return for interest on your money. This is one of the best savings accounts in which you can invest. Investing your money in a CD is safe because they are FDIC insured. The Federal Deposit Insurance Corporation (FDIC) insures your CDs for as much as $250,000. As long as you do not invest more than $250,000 into your CD, you will not lose your principal if something happens to the bank.

Higher Interest Rates

CDs tend to have a higher interest rate than your average checking and savings accounts and money market accounts. Most financial institutions offer CDs with varying rates, so it is in your best interest to research the best rates. You may be able to find a higher interest rate from an online bank. These banks have less overhead and tend to pass those savings along to their customers in better interest rates. You also want to understand how the banks compounds the interest on CDs. If the interest is compounded daily, your CD will gain more interest.

There are different types of CDs available. There are fixed-rate CDs and variable-rate CDs. The fixed-rate CD is locked in for the entire length of your term. A variable-rate CD goes up and down based on the banks rates which change based on the market changes. Many CDs do not have fees, or they have low fees.

What Are the Negatives about CDs?

There are some negatives to a CD. There are way more benefits than there are negatives, but you should still be aware of the negatives. This way you can make an informed choice about the best savings accounts for you.

Unable to Invest Elsewhere

One downside of a CD is the money you put in the CD remains there for as long as the term states. If the term of the CD is five years, then you cannot touch that money for five years. If you decide to take the money out of the CD, you are hit with penalties. While your money is sitting in the CD, you are not able to invest that money elsewhere. Typically, CDs do not increase with time to match the rate of inflation.

What Should I Know about Managing Money?

Before you begin looking for the best savings accounts for you, you should understand a bit about managing money. The most basic definition of money management is tracking your spending and comparing it to your income. It means creating a budget and sticking to it. It means understanding the needs of your household and ensuring your budget allows for those needs. In its simplest terms, it is how to be better with money. I will talk more about creating a budget lower in this article, but there are some other basics you should understand about managing your money.

You should have an understanding of your expenses and how you spend your money. When you have a grip on this, you have an understanding of financial management.

Pay Your Bills

You should make sure that you pay your bills on time. This helps to make sure you stay on top of your bills and pay them timely.

Keep a Good Credit Score

This is also a great way to maintain a good credit score. One of the top reasons your credit score decreases is as a result of late or missed payments.

Pay Your Taxes

You should also make sure you pay your taxes. The last thing you want to do is have the IRS hunting you down for money. The federal government always gets its money, so you should make sure that you make arrangements to pay your taxes.

What About Credit Cards?

I cannot talk about managing money without discussing credit cards. When you begin thinking about the best savings accounts, you also need to consider your credit cards. On one hand, a credit card can allow you some freedom with your expenses and money.

Be Smart about Using Your Credit Cards

However, you have to maintain a sense of self-control and pay attention to your spending. When you are given the flexibility of a credit card, it is easy to lose control of your spending. It truly comes down to you and whether or not a credit card can be a wonderful addition to your money management plan.

Credit cards often have high interest rates, higher than you can find from a personal loan. If you only pay the minimum payment, you will not be able to pay down your credit card debt. You will find yourself in a cycle of never being able to pay down your credit card debt because the minimum payment is only enough to pay the interest that accumulates from month to month.

Keep your goals in mind whenever you use your credit cards. If using them is going to move you further away from your goals, then maybe you should decide not to use them.

Do I Need A Budget?

Yes, you absolutely need a budget. Even the best savings accounts in the world can help you save money if you do not put anything in the account. If you do not currently have a budget, you should use one of the many websites to help you create one. Not only is having a budget an important tool to help you save money, but it also puts you in control of your spending. Once you have a clear understanding of your spending as it compares to your income will you know how much you can save.

Create a Budget

The simplest way to determine this is to put your income in one column and list all of your expenses in a second column. Then you add up all of your expenses. Once you added up all of your expenses, you subtract your expenses from your income and that is how much money you have each month to save or spend. Just to warn you, this tends to be an eye-opening experience. Most people are not aware of how much money they spend. They also are not aware of how much money they are spending that they do not really have.

Are There Other Ways To Save Money?

I am sure that you do not want to hear this but the best way to save money is to cut spending. When you cut spending, you have more money to put into the best savings accounts. In the step above, you listed out all of your expenses. Now that you see them in black and white, it is easy to see where you are spending your money.

The first and easiest things to cut are the items you are not using. That gym membership is a great example. If you have a gym membership that you are not using, cancel it. Stop everything and cancel it right now. It is wasting your money. You could be saving that money.

If you have any other subscription services that are automatically debited from your account, take a look at them. The first question you should ask is do you need or want them? If no, then cancel those services. If yes, take a look at how often you receive them. Can you reduce the amount of time? Can you change it so that you request it manually and it does not just ship? This way you can control how often it comes and only receive a shipment when you need it.

I do not know about you, but I find I never get it right. If I have something automatically delivered to me, I end up with way more than I need. I am constantly adjusting it and playing with how often it is shipped to me. You should make those adjustments so that you do not have a surplus.

Conclusion

I have given you a lot of information about the best savings accounts. This information is just a starting point. You should do some research about the ten savings accounts I listed. They all have something a little different to offer you. Some have really high interest, but also require a high balance. Some of the banks are online only.

Make sure you understand your needs when it comes to a savings account. This can help you narrow down your options and find the best one for you. Also, keep in mind opening a savings account is only half the battle. You also need to put money in there so it can grow. Create a budget and find ways to cut spending so you can save more money.